The first question most people have after they get a will is where they should keep it. It’s a good question to ask because you need a place that’s both safe and accessible for your important documents. It needs to be a safe location so they won’t get stolen or destroyed. But it also needs to be accessible so you (or your loved ones) can easily get to the documents when they’re needed.

The first question most people have after they get a will is where they should keep it. It’s a good question to ask because you need a place that’s both safe and accessible for your important documents. It needs to be a safe location so they won’t get stolen or destroyed. But it also needs to be accessible so you (or your loved ones) can easily get to the documents when they’re needed.

The Problem with a Safe Deposit Box

The first place that comes to mind for most people is to get a safe deposit box and keep their important documents there. The problem is that a safe deposit box can be a nightmare to get into after you die. If your box isn’t held jointly with someone who’s still alive after you die (or held in the name of your revocable living trust), then it’ll take a court order to open your safe deposit box and get to your documents. This can mean delays and headaches for your loved ones.

You can avoid this by adding a joint owner you trust to your safe deposit box. Alternatively, you can make your revocable living trust the owner and your successor trustee will be able to access the box on your behalf. But you’ll want to make sure the trust document isn’t in the box, or your successor won’t be able to prove he has legal access!

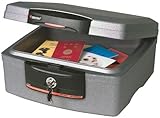

The Fireproof and Waterproof Safe

My personal choice is the fireproof and waterproof safe. They’re affordable and will protect your documents well. I found this SentrySafe Fireproof and Waterproof Safe on Amazon for $39.97:

It’ll protect your documents from fire for half an hour at temperatures up to 1,550 degrees Fahrenheit and has a waterproof seal as well. (I wonder if it can protect from fire and water at the same time???) However, it’s not theft-proof. The lock could be opened by a thief who really wants it and it’s only 25 pounds. If theft is something you’re worried about, you can bolt your safe to the floor or wall with some hardware and tools. It’ll at least discourage the thief from trying too hard.

The main caution with this option is to make sure someone else knows where the safe is and how to open it. Obviously, this should be someone you trust. The upside to using your own safe is that it will be easy to access whenever you need it.

At a Minimum…

If you don’t want to get a safe deposit box or a home safe, you should at least keep your important documents on a high shelf. It won’t protect them from fire, but it may save you from some water damage. Also, make sure you and anyone who cleans around your house knows they’re important. You wouldn’t want to throw them in the trash accidentally!

Have a Financial Question?

This post was written to answer a reader request. Have a financial question you’d like answered? Contact me and I’ll help you as best I can!

(photo credit: Cliff on Flickr)

This article was included in the Carnival of Personal Finance.

My youngest sister will be having a baby soon. We were discussing wills recently, and she wisely brought up the question of how to choose a guardian for your child. I gave her some basic tips in an email, but I thought it would make a good topic for a post. This is an expansion of the advice I gave my sister.

My youngest sister will be having a baby soon. We were discussing wills recently, and she wisely brought up the question of how to choose a guardian for your child. I gave her some basic tips in an email, but I thought it would make a good topic for a post. This is an expansion of the advice I gave my sister.