Beginning February 22, 2010, banks and credit card companies had to start complying with the Credit Card Accountability, Responsibility and Disclosure Act (Credit CARD Act). (Who comes up with these names???) Here’s a summary of the new rules.

Interest Rate Increases

Credit card companies cannot increase your rate for the first 12 months after you open an account. But, as always, there are exceptions:

- If your card has a variable interest rate tied to an index, your interest rate can go up whenever the index goes up.

- If your card has an introductory rate, it must be fixed for 6 months. After that, your rate can go to whatever the company disclosed when you got the card.

- Your rate can go up if you are more than 60 days late paying your bill.

- Your rate can also go up if you’re in a “workout” agreement (debt management plan) with the credit card company but don’t pay as agreed.

If your interest rate increases after the first year, the new rate will only apply to new charges you put on your card. Your old interest rate will still apply to any balance you have after that time.

Also, credit card companies are required to give you 45 days notice before they raise your interest rate, change certain fees, or make other significant changes to the terms of your credit card. They must then give you the option to cancel the card before the increases take effect.

If you decide to cancel the card, the company may close your account and require you to make higher payments. They can require you to pay off the remaining balance within five years. Or they can double the percentage required to make your minimum payment. Either option will result in a faster repayment of your credit card debt.

But once again, there are exceptions to the 45 days notice rule. The credit card company doesn’t have to notify you if:

- you have a variable interest rate tied to an index and the index goes up.

- your introductory rate expires and increases to the rate described when you opened the card.

- your rate increases because you fail to make the payments agreed to in your “workout” agreement.

Changes to Your Statement

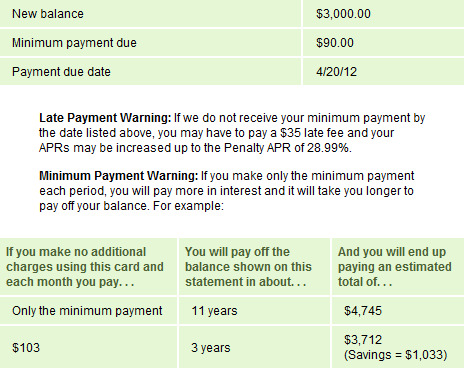

Credit card companies must now begin including information on how long it will take to pay off your credit card with every billing statement. I’ve already seen this change on my credit card statements, and I think it’s a good thing. I don’t know if people will actually read it, but at least the information is there for them to see. Companies must tell you how long it will take to pay off your card if you only make the minimum payment and how much your payment should be to pay it off within 36 months. Here’s an example of what this information will look like:

Over-limit Transactions

The new rules require you to opt-in to over-the-limit transactions if your credit card company wants to charge you an over-limit fee. If your credit card company lets a transaction go through that puts you over the limit, they can’t charge you an over-limit fee unless you opted in.

Even if you do opt-in to over-limit transactions, the credit card company can only charge you one over-limit fee per billing cycle. You can always opt-out at any time.

Caps on Fees

If your credit card company requires you to pay fees for the “privilege” of using their card, those fees cannot total more than 25% of the initial credit limit. So if you start out with a credit limit of $2,500, the company cannot charge you more than $625 in fees for the first year. Penalty and late payment fees do not count toward this limit.

Personally, I don’t think this is going to change much of anything. If credit card companies want to charge you a high fee, all they have to do under this rule is give you a larger initial limit.

New Rules if You’re Under 21

If you’re under 21, you’ll have to show that you can make the payments yourself (whatever that means…) or have a cosigner before you can open a credit card. Additionally, if you have a cosigner and want to increase the limit on your card, the cosigner must agree to the limit increase in writing.

There are also some rules on where credit card companies can market their cards (around college campuses) and what incentives they can offer to students. Again, credit card companies will find ways around these rules so they’re useless in my opinion. (except for the credit limit increase…that might be good)

Payment Due Dates and Times

Credit card companies must deliver your billing statement at least 21 days before your payment is due. Additionally, your payment due date must always be the same date each month. (For example, always on the 15th of the month or always on the last day of the month.) The payment cutoff time cannot be any earlier than 5 PM on the due date. And if your due date falls on a holiday or weekend, you have until the next business day to make your payment.

How Your Payments Are Applied

If you ever pay more than the minimum payment, your credit card company must apply the extra toward your balances with the highest interest rate first. However, if you bought something under a “deferred interest plan” (you know, “no interest until…”), then there’s an exception. First, you may choose to apply your extra payments to the no interest balance first. Second, if you’re within two months of the end of your no interest period, then your credit card company must apply your entire payment to the no interest balance. This is to keep you from getting socked with hidden interest fees if you don’t pay it off by the end of the promotional period.

No Two-cycle Billing

Credit card companies can only charge interest on balances in your current billing cycle. Two-cycle billing was a nasty trick that should have been outlawed as soon as it came out – but no one made you agree to it either. Doesn’t matter any more though since companies can’t use that billing method anymore.

Questions?

That covers the basics of the Credit CARD Act. If you have any questions, let me know in the comments!

Container gardening is a great choice if you have limited space or limited desire to garden. It doesn’t take much time and you don’t have to worry about weeds. But you still get to enjoy the vegetables of your labor. You can use just about any container you can get your hands on (as long as it won’t leach poisonous chemicals into the soil). It doesn’t even need to be very deep – you can grow quite a bit of stuff in just six inches of soil. (I know. I’ve done it!) You’ll just need a few holes in the bottom for drainage. You can find cheap options for containers by looking creatively around your house, going to yard sales, or stopping by your local thrift store.

Container gardening is a great choice if you have limited space or limited desire to garden. It doesn’t take much time and you don’t have to worry about weeds. But you still get to enjoy the vegetables of your labor. You can use just about any container you can get your hands on (as long as it won’t leach poisonous chemicals into the soil). It doesn’t even need to be very deep – you can grow quite a bit of stuff in just six inches of soil. (I know. I’ve done it!) You’ll just need a few holes in the bottom for drainage. You can find cheap options for containers by looking creatively around your house, going to yard sales, or stopping by your local thrift store. Raised beds are just a variant of container gardening. Put a few boards together with screws, cover the ground with landscaping cloth (to reduce weeds), and throw in some soil. Now you’ve got one giant container for your garden. It should be at least six inches deep, and you’ll need somewhere to put it. Full sun is best, but you can grow all sorts of vegetables in partial shade. If you find you need to grow more stuff but don’t want to rip up your yard, you can just build another raised bed. Easy expansion!

Raised beds are just a variant of container gardening. Put a few boards together with screws, cover the ground with landscaping cloth (to reduce weeds), and throw in some soil. Now you’ve got one giant container for your garden. It should be at least six inches deep, and you’ll need somewhere to put it. Full sun is best, but you can grow all sorts of vegetables in partial shade. If you find you need to grow more stuff but don’t want to rip up your yard, you can just build another raised bed. Easy expansion! This is the typical image that comes to mind when we talk about gardening – a rectangular piece of ground that’s been tilled up and is ready to plant. This option can require the most work and/or money. You don’t have to buy the soil, but you’ll probably need to add something to it and you’ll have to work it. Oh, and you’ll need the space and willingness (or permission) to tear up a patch of your yard!

This is the typical image that comes to mind when we talk about gardening – a rectangular piece of ground that’s been tilled up and is ready to plant. This option can require the most work and/or money. You don’t have to buy the soil, but you’ll probably need to add something to it and you’ll have to work it. Oh, and you’ll need the space and willingness (or permission) to tear up a patch of your yard!