A while back I released my free retirement calculator designed to take your current age, retirement age, life expectancy, income needs, current savings, and market volatility into account in order to tell you how much you should be saving each year to reach your retirement goals. I designed it to be a more accurate retirement calculator than most of the ones you find online, but I also wanted to make it easy to use. Because of this, it’s not the most accurate calculator available, but it should do a good job for you if you follow the directions and revisit it every 3-5 years.

What I hadn’t done, though, was to test the advice it gives against historical investment periods. I based the calculator on historical market data and ran millions of simulations to build the back-end of the calculator (which you don’t see when you use it). But I didn’t have a chance to test how it would have actually worked out for people until recently. So using historical performance numbers for a diversified portfolio along with historical inflation rates (all from 1927-2009), I tested what your results would have been if you had followed the advice given by my free retirement calculator. I tested two different scenarios:

- If you had saved the target amount the calculator estimates, would that have lasted throughout your retirement?

- If you had annually saved the amount the calculator tells you to, would you have reached that target amount by your retirement date?

Basically, I wanted to see if this calculator would work in telling you how much to save and how much you can safely withdraw in retirement. Click here if you don’t want to read the nitty gritty and just want to get to the point.

Withdrawal Results

I found that my calculator was extremely good at estimating how much you should have by retirement so you don’t run out of money before you die. What I wanted to avoid was having any historical period where you would have run out of money before you hit your life expectancy. In most cases, you end up with quite a bit of money left over at your death. But in a few, you barely make it. All of these withdrawal scenarios assume you need $36,000/year in retirement income and you retire at age 65. I looked at three different scenarios: you die at age 85 (20 years of withdrawals), you die at age 80 (15 years), and you die at age 75 (10 years). You’ll need to click the graphs to get a clear, full-size picture. Here are the results for withdrawing from age 65-85 (20 years):

Here are the results for 65-80 (15 years):

And here are the results for 65-75 (10 years):

As you can see, you never would have run out of money if you had saved what the calculator estimated you would need. Now there’s no guarantee that would always be true, but it is good to see that it would have worked out historically. In many cases, you would have ended up with way more money than you needed, which illustrates why this isn’t a perfect calculator. (No calculator is going to figure this out perfectly for you, and this is why you have to revisit the calculation every so often.)

Savings Results

Where I found the calculator needed some work was how much it was telling you to save every year. I was running a scenario where you start saving at age 25, retire at 65, and die at age 85 (40 years of saving, 20 years of withdrawals). What I found was that many times you’d end up with waaaaaay more than you needed to retire. You could have either retired earlier or saved less. This kind of result is almost as bad as finding out you didn’t save enough – simply because of all the sacrifices you would have made to meet your savings goal. I don’t have the results here to show you, but let’s just say you ended up with anywhere from 2-6 (yes 6!) times what you would have needed to retire.

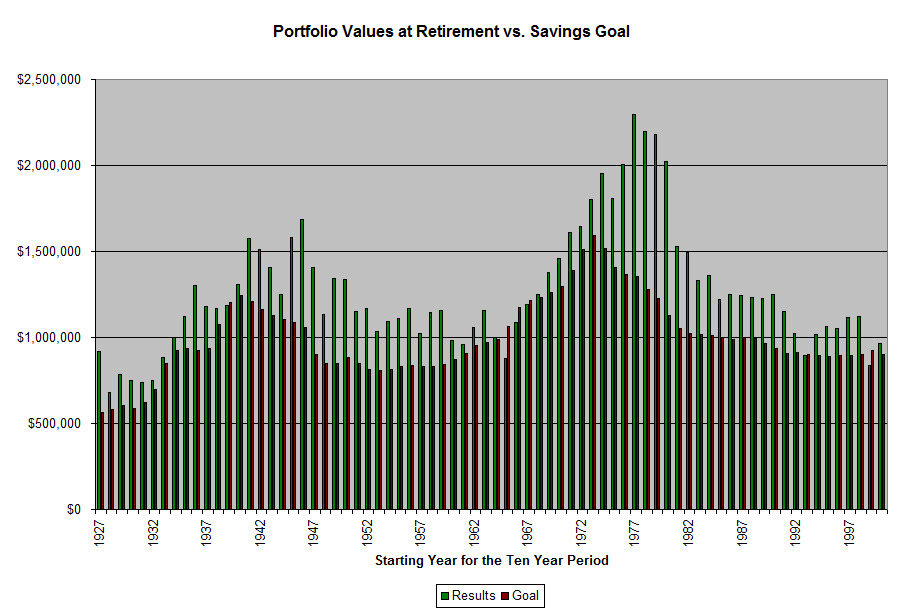

After a long process of studying the results, figuring out where it went wrong, debugging, and retesting, I made one small tweak to the calculator and now it works great. Historically speaking, you’d still save too much most of the time (anywhere from 1.25 to 2 times more than you need). But it cut the required savings rate back to a much more manageable and realistic level. So I’ve run four different scenarios and included the results here to show you how it worked out. These scenarios assume you retire at age 65 and die at age 85 while needing $36,000/year during retirement. The four scenarios differ in the age you start saving (with no savings to start): age 25 (40 years to save), age 35 (30 years), age 45 (20 years), and age 55 (10 years). Here are the results if you start at age 25:

On average, you would have saved about 50% more than necessary. Assuming you have 40 years to save, nothing in savings, and you’ll be in retirement for 20 years, you need to be saving 15% of your target retirement income every year. Here are the results if you start at age 35:

On average, you would have saved about 50% more than necessary once again. Assuming you have 30 years to save, nothing in savings, and you’ll be in retirement for 20 years, you need to be saving 29% of your target retirement income every year. Here are the results if you start at age 45:

On average, you would have saved about 50% more than necessary once again. You would have fallen a little short of your retirement goal 8 times out of 64 historical 20 year periods, which would have required you to retire on a slightly smaller retirement income or wait one more year to retire. Assuming you have 20 years to save, nothing in savings, and you’ll be in retirement for 20 years, you need to be saving 63% of your target retirement income every year. And here are the results if you start at age 55:

On average, you would have saved about 30% more than necessary. You would have fallen just short of your retirement goal 6 times out of 74 historical 10 year periods, which would have required you to retire on a slightly smaller retirement income or wait one more year to retire. Assuming you have 10 years to save, nothing in savings, and you’ll be in retirement for 20 years, you need to be saving an astounding 170% of your target retirement income every year.

Though it’s not necessary to get the point of this article, I threw in those required savings amounts to show you why you need to start saving for retirement early in life. If you start at age 25 (when you have 40 years to invest), you only need to save 15% of your target retirement income every year. But if you wait until you’re 45 or 55, you’re looking at 60-170%. Ouch!!! Start early and save yourself from scrambling at the end!

The Point

While it worked great for withdrawals (during retirement), I’ve made the retirement calculator a bit more accurate and realistic while you’ll be saving – especially if you follow the instructions and run through the calculations again every 3-5 years. I hope you find it useful. If you have any questions, please feel free to leave them in the comments here or on the calculator’s page. Thanks!

If you enjoyed this, you might like:

- 5 Things to Think of Before Retiring

- The Root of Riches: Interview with Chuck Bentley, CEO of Crown Financial Ministries

- Tax Tip: Combine a Traditional IRA Deduction with the Retirement Savings Contribution Credit

- The 80% or 90% of Income for Retirement Rule Is Stupid

- The Save 10% for Retirement Rule Is Stupid